1. Introduction: The Cash Flow Trap

It’s the classic paradox of running a B2B business. You just landed the big contract. The work is complete, the service is delivered, and the invoice has been sent. On paper, you are crushing it.

But your bank account? It hasn’t seen a dime.

Your cash, the lifeblood of your operation, is locked up in that invoice for 30, 60, or even 90 days. You have payroll to meet, suppliers to pay, and new opportunities to fund. This is the “cash flow trap.” You’re profit-rich, but cash-poor, and it’s one of the most frustrating places to be.

How do you pay this week’s bills with next month’s money?

You don’t. You unlock it.

This is the power of invoice financing. Forget the idea of a traditional, red-tape-filled bank loan. This isn’t about taking on new debt. Think of it as a strategic lever. It’s a way to access the working capital you have already earned, giving you a powerful tool to control your company’s financial rhythm.

- What is invoice financing?

Invoice financing lets businesses get an immediate cash advance (typically 80-90%) against their outstanding B2B invoices.

- What’s the difference between factoring and discounting?

- Invoice Factoring: You sell your invoices to a financier. They manage collections, and your customers know (this is disclosed).

- Invoice Discounting: You borrow against your invoices. You manage collections yourself, and your customers don’t know (this is confidential).

- Which one should I choose?

- Choose Factoring if: You need help with collections/admin and are okay with disclosure.

- Choose Discounting if: You need confidentiality and have strong internal credit control.

- Average Cost: 1-5% of the invoice value

- Funding Speed: 24-48 hours

1.1 Who This Guide Is For

If any of these sound familiar, you’re in the right place:

- B2B business owners are tired of waiting 30 to 90 days for payment.

- SME founders who need to pay their own suppliers before getting paid by clients.

- Finance managers are looking for scalable, non-dilutive funding to manage working capital gaps.

1.2 What You’ll Learn

We’ll cut right to the chase. In this guide, you’ll learn:

- What invoice financing actually is (and what it isn’t).

- The critical, must-know difference between Factoring and Discounting.

- When to use each method (with clear, practical examples).

- How to qualify for it and what to look for in the right partner.

- The real talk: a breakdown of the benefits, the risks, and the costs.

2. What Is Invoice Financing?

Invoice financing is a financial tool that allows a business to get an immediate cash advance by using its outstanding customer invoices (known as accounts receivable) as collateral.

It’s a powerful way to unlock working capital that is tied up in unpaid invoices. Instead of waiting the standard 30, 60, or even 90 days for a customer to pay, you can access the majority of that cash almost immediately, giving you the funds to pay staff, buy supplies, and fuel growth.

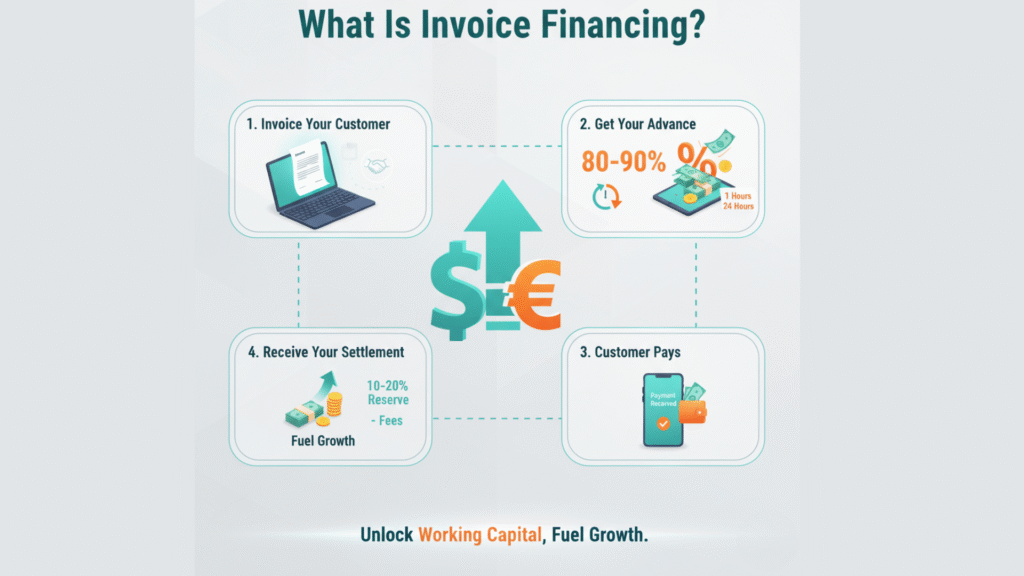

2.1 How Does Invoice Financing Work? (The 4-Step Process)

While providers may differ slightly, the process generally follows four simple steps:

- Invoice Your Customer: You provide your goods or services to your customer and issue an invoice for the work, just as you normally would.

- Get Your Advance: You “sell” or assign this invoice to the invoice financing company. They will then quickly advance you a large percentage of the invoice’s value, typically 80% to 90% often within 24 hours.

- Customer Pays the Invoice: They pay the full invoice amount, just as agreed. Depending on your setup (factoring/discounting), the cash either goes straight to the financier or lands in a special account in your name.

- Receive Your Settlement: Once the financier receives the full payment, they remit the remaining balance (the 10% to 20% held in reserve) back to you, minus their agreed-upon service fee.

2.2 Key Distinction: Why Invoice Financing Is Not a Traditional Loan

Don’t get it twisted: This gives you cash, yes, but A/R financing is a totally different animal than a regular bank loan or overdraft.

- It’s Not New Debt: You aren’t creating a new liability on your balance sheet. You are simply accessing the cash value of an asset you already own, your unpaid invoice.

- It Scales With Your Sales: A bank loan gives you a fixed lump sum. Invoice financing is flexible; the amount of funding available grows directly as your sales and invoicing increase.

- The Invoice is the Collateral: Forget trying to pledge the company van or your fancy office chairs. With this, the invoice itself is the security. This is a game-changer if your business is rich in great clients but poor in “big, expensive stuff” that a traditional bank would want.

3. The Two Pillars: Factoring vs. Discounting (The Critical Choice)

You’ve decided invoice financing is right for you, but now comes the most important decision: Which type do you choose?

The entire difference between Invoice Factoring and Invoice Discounting boils down to answering two simple, but critical, questions about your business:

- Do you want your customer to know you’re using a financier? (Confidentiality)

- Do you want to manage your own payment collections? (Control)

Your answers to those questions will guide you to one of the two main solutions: the Full-Service Solution or the Confidential Solution.

3.1. What is Invoice Factoring? The “Full-Service” Solution

Invoice Factoring is a financial service where your business sells its unpaid customer invoices to a third-party financier (a “Factor”) at a small discount.

In simple terms: Instead of waiting 30, 60, or 90 days for your customer to pay, you get the majority of that cash now. Crucially, the Factor typically takes over your collections process, saving you time and administrative hassle. You get cash quickly, and you outsource the job of chasing payments.

Think of Invoice Factoring as outsourcing your entire Accounts Receivable department.

| Feature | Description |

| How it Works | The financier buys your invoices and takes over your sales ledger. |

| Collections | The financier is responsible for credit control and actively chases payments from your customers. |

| Confidentiality | Disclosed. Your customer is informed and pays the financier directly. |

- Pros

- Outsourced Collections: This is a huge time-saver! You offload the entire administrative burden of chasing slow payments.

- Bad Debt Protection: Often available as “Non-Recourse Factoring,” where the financier takes the loss if the customer defaults (though this is more expensive).

- Cons

- Customer Visibility: Because the financier steps in to manage collections, your customers will be aware that a third party is involved in your financing.

- Added Expense: You’re covering the cost of a full-service team that handles both administration and collections, so the fees tend to be higher.

3.2 What is Invoice Discounting? The “Confidential” Solution

Invoice Discounting is a smart financial strategy where you use your unpaid customer invoices as collateral to get a quick cash advance, typically 80% to 90% of the invoice value.

Here’s the most important part, the reason businesses choose it: You remain in complete control. Invoice Discounting is the option for businesses that want funding but need to keep their financing arrangements completely private.

Your customers are not informed of the arrangement. You manage the collections, chase payments, and maintain your direct, confidential relationship with your client, all while enjoying immediate access to the cash that was stuck in a 60 or 90-day payment cycle.

In simple terms, it’s like a confidential loan secured by your receivables. You get the funding, but your business operation looks the same to your customers.

| Feature | Description |

| How it Works | The financier lends against your invoices, which act as collateral. |

| Collections | You remain in control. You manage your own sales ledger and chase payments just as you always have. |

| Confidentiality | Confidential/Undisclosed. Your customer is completely unaware of the arrangement. |

- Pros

- 100% Confidentiality: It preserves your professional image and maintains your direct, uninterrupted customer relationship.

- Lower Fees: Since you’re handling all the administrative work, the financier’s fees are generally lower.

- Cons

- Collections Responsibility: You must have a robust internal accounts team because you are still responsible for chasing all payments.

- Risk (Recourse): It’s usually “Recourse,” meaning if your customer defaults or doesn’t pay, you are liable and must repay the advance to the discounter.

3.3 Head-to-Head: Factoring vs. Discounting (The Critical Comparison)

| If You Need… | Your Best Choice Is… | Why? |

| Help with collections & admin | Factoring | You’re essentially hiring a collections team. |

| 100% confidentiality | Discounting | Maintains your image and customer relationship. |

| Bad debt protection | Factoring (Non-Recourse) | The factor assumes the credit risk of your customer. |

| Full control of customer relations | Discounting | You are the only point of contact for payment. |

3.4. Decision Tree: Which One is Right for You?

If you’re still on the fence, use this quick guide to determine the best path forward.

| Question | If YES… | If NO… |

| 1. Do you have a strong in-house accounts team capable of collections? | Consider Discounting. You can handle the admin and save on fees. | Consider Factoring. Outsource the collections headache and save time. |

| 2. Is customer confidentiality critical to your brand or contracts? | Discounting only. You cannot risk your customer knowing. | Either works. Confidentiality isn’t a primary barrier. |

| 3. Do you want protection against bad debt (customer non-payment)? | Non-Recourse Factoring. This transfers the risk to the financier. | Recourse Discounting or Factoring. You accept the risk for a lower fee. |

4. Real-World Scenarios: Factoring vs. Discounting in Action

Scenario 1: The Manufacturing SME (The Need for Admin Help)

The Business: A textile manufacturer that supplies over 100 small to medium-sized retail clients (a high volume of small invoices).

The Problem: Their small accounts team is completely snowed under. They’re spending all day playing collections agent, hounding customers for payments. This means they have zero time left for their actual jobs, managing costs, sorting out production, and helping the business grow. All that chasing has become a massive clog in the drain.

The Solution: Invoice Factoring (The Full-Service Model)

- Why it Fits: The manufacturer’s biggest problem is time and administrative burden.

- Result: They sell their invoices to the factor. The factor handles all credit control, sends collection letters, and follows up on every payment. The manufacturer gets immediate cash, and its small team is freed up to focus entirely on core manufacturing and sourcing, effectively outsourcing a non-core headache.

Scenario 2: The Established B2B Service Agency (The Need for Confidentiality)

The Business: A reputable IT consultancy that works with a few large, blue-chip corporate clients (a low volume of high-value invoices).

The Problem: We finally won the huge client fantastic! But now we have a huge, immediate payroll deadline, and their payment terms are a painful 120 days. We need cash now. And here’s the kicker: we absolutely cannot let them know we’re borrowing, or they’ll think we’re broke. Keeping up appearances is non-negotiable.

The Solution: Confidential Invoice Discounting (The Control Model)

- Why it Fits: The primary need is confidentiality and maintaining the client relationship.

- Result: The financier quietly provides the needed funds, keeping everything discreet. The IT agency stays in charge of its own accounts and continues to follow up on payments directly. The high-profile client pays the agency just like always, unaware of any changes so the trusted relationship stays intact. Meanwhile, the agency gets the breathing room it needs to handle payroll without a hitch.

Scenario 3: The MSME Government Contractor (The Regulated Model)

The Business: An IT vendor classified as an MSME (Micro, Small, or Medium Enterprise) that wins a ₹50 lakh government contract.

The Problem: Government entities and PSUs often have very long, rigid payment cycles (e.g., 90 to 120 days), but the vendor needs cash now to pay suppliers and take on the next contract.

The Solution: Trade Receivables Discounting System (TReDS)

- Why it Fits: TReDS is the RBI-approved digital fix for MSME cash flow. It instantly turns your big-buyer invoices especially those from government or PSUs, into immediate funds. It’s simple, secure, and kills those brutal payment delays so your business keeps moving.”

- Result: The vendor uploads the confirmed invoice to TReDS. Multiple financiers (banks/NBFCs) competitively bid on it. The vendor chooses the best bid, gets an 80-85% advance in as little as 48 hours, and most importantly, these transactions are typically without recourse to the MSME, meaning the risk of buyer default is transferred to the financier. This allows the MSME to immediately scale its business.

Summary: Your Business Needs Dictate the Choice

| Business Type & Need | The Problem | The Best Solution | Key Feature Addressed |

| Manufacturer/Wholesaler | Too many invoices to manage; needs to outsource collections. | Invoice Factoring | Outsource Administration |

| Consultancy/Agency | Financing big-name clients; must maintain confidentiality. | Invoice Discounting | Preserve Customer Relationship |

| MSME/Govt. Supplier | Very long, rigid payment cycles from large entities. | TReDS Discounting | Regulated, fast, and often Non-Recourse |

Ready to Unlock Your Cash Flow?

You’ve seen how factoring and discounting work. If you, like the businesses above, need a confidential, fast, and transparent way to fund your invoices, MRKN can help.

We specialize in confidential invoice discounting for B2B businesses and MSMEs.

Schedule Your Free Cash Flow Analysis

5. How to Get Invoice Financing: A 4-Step Action Guide

Want to turn your invoices into quick cash? Getting invoice financing is usually much faster and simpler than going through a traditional loan process. Here’s how to get started step by step:

Step 1: Assess Your Needs (Factoring vs. Discounting)

Before you approach any financier, you must clarify your goal (based on Section 3):

- Need for Confidentiality? If maintaining the client relationship is paramount and you have a solid in-house collections team, prioritise Invoice Discounting.

- Need for Collections Help? If you have a small accounts team that is overwhelmed with chasing payments, prioritise Invoice Factoring to outsource that administrative work.

Step 2: Check Your Eligibility – What Lenders Look For

The great thing about invoice financing is that eligibility often hinges more on your customers’ creditworthiness than on your own company’s net worth or assets. Lenders will primarily evaluate three things:

- Customer Creditworthiness (Most Important): The financier needs assurance that the invoice will be paid. They will often run credit checks on your major clients.

- Your Invoicing Process: Your invoices must be clear, undisputed, and for confirmed goods/services already delivered. Clean, professional invoicing is a must.

- Your Business Track Record: They will review your sales ledger, debt history, and basic financials to confirm stability, but the focus remains on the quality of your sales.

Step 3: Prepare Your Documentation

Getting your documents ready streamlines the approval process. You should prepare:

- Sales Ledger: A comprehensive list of your current outstanding accounts receivable.

- Sample Invoices: A few recent, high-value invoices to show the clarity of your billing.

- Business Financials: Basic P&L statements or bank statements to establish credibility.

- Legal/KYC Documents: Standard business registration and identity proof.

Step 4: Compare Providers and Decode the Real Cost

This is where many businesses make a mistake! The “headline rate” can be deceptive. Invoice financing costs are structured differently from a loan, so you must look at the Total Cost of Funds.

- Real Cost Example: What You’ll Actually Pay

Let’s look at a ₹10,00,000 invoice to see how the various fees stack up:

| Invoice Financing Breakdown | Amount (₹) | Notes |

| Invoice Value | ₹10,00,000 | The full amount your customer owes. |

| Initial Advance (85%) | ₹8,50,000 | The cash you get immediately. |

| Discount Fee (2% of Invoice Value) | ₹20,000 | The primary interest/finance fee for the service. |

| Service Fee (Admin/Monthly Fee) | ₹5,000 | Covers administrative costs and ledger management. |

| Net You Receive (Initial Advance – Fees) | ₹8,25,000 | The cash in your bank account today. |

| Customer Pays Full Invoice | ₹10,00,000 | Paid to the financier (or your designated account). |

| Final Settlement | ₹1,25,000 | The reserve (₹1,50,000) minus the fees (₹25,000). |

In this example, the total cost for the funding period is ₹25,000.

- Hidden Fees to Watch Out For

To avoid nasty surprises, always ask your potential financier to disclose all of the following:

| Fee Type | Description |

| Setup/Origination Fees | A one-time charge to get your account activated. |

| Monthly Service Minimums | A minimum fee you must pay, even if you don’t use the service much that month. |

| Per-Invoice Processing Fees | Small fees (e.g., ₹100-₹500) are charged every time you submit an invoice. |

| Bad Debt Protection Fees | The cost for using Non-Recourse Factoring (where the financier takes the default risk). |

| Early Termination Penalties | Penalties if you decide to end the agreement before the contract term is over. |

By focusing on the all-in cost and being prepared with your documentation, you can efficiently secure the right invoice financing solution to smooth out your cash flow.

6. The 360° View: Benefits, Risks, and Market Trends

6.1 For Your Business: The Pros vs. Cons

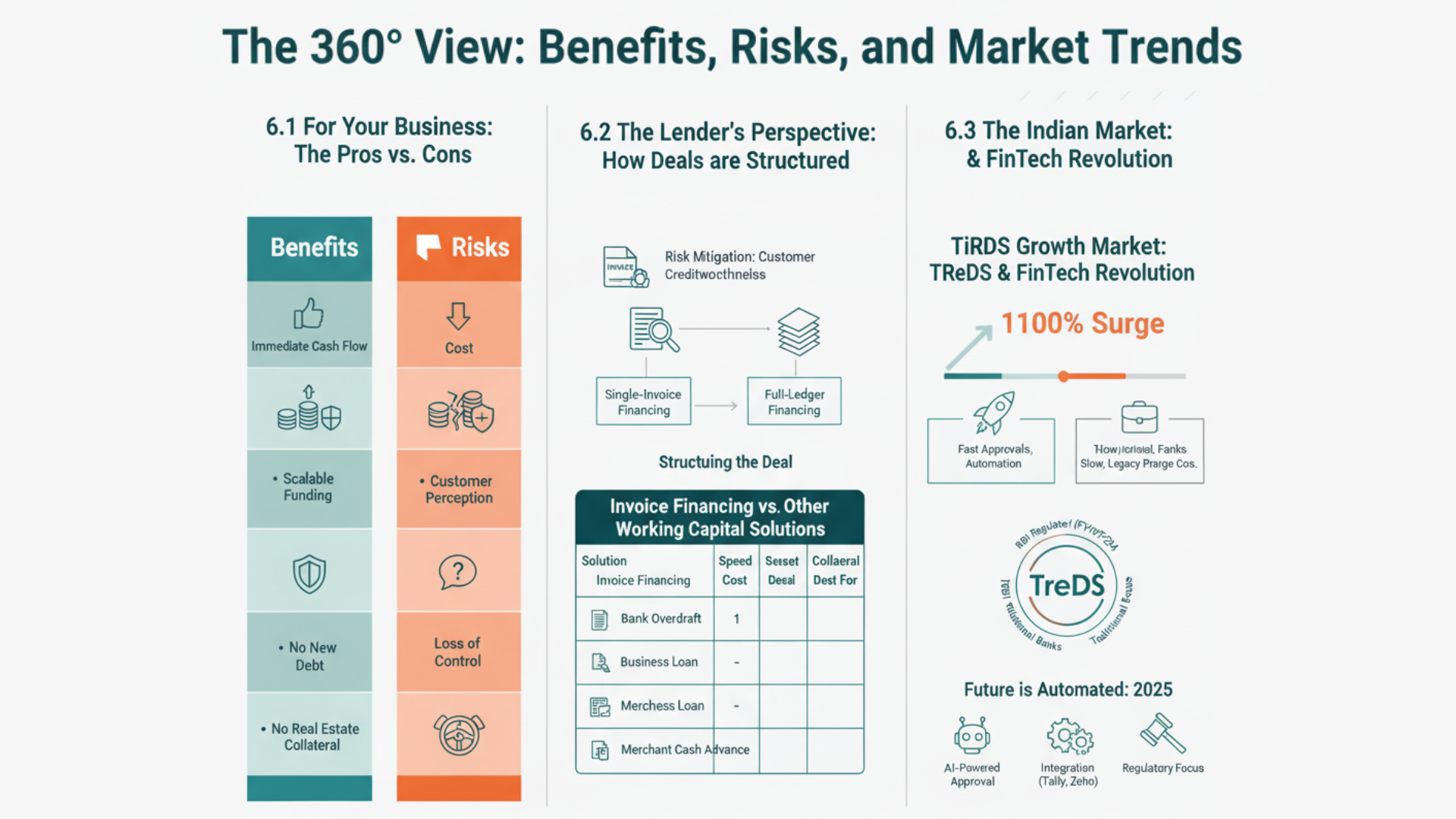

Invoice financing is a powerful tool, but like any financial instrument, it comes with trade-offs. Here is a balanced look at the advantages and disadvantages:

| 👍 Benefits (Pros) | 👎 Risks (Cons) |

| Immediate Cash Flow: Get the cash tied up in your invoices in as little as 24-48 hours, drastically improving liquidity. | Cost: Can be significantly more expensive than a traditional, long-term bank loan or overdraft facility. |

| Scalable Funding: Unlike a traditional loan, the funding you receive expands automatically as your sales and invoice volume rise. | Recourse Risk: In “with recourse” agreements, which are often seen in discounting, if your customer fails to pay, you’re responsible for covering that bad debt. |

| No New Debt: It is the sale of an asset (your invoice) or a secured advance; it typically does not appear as new debt on your balance sheet. | Customer Perception: (Primarily for Factoring) The financier handles collections, which can occasionally impact the relationship or perception of financial stability if not managed tactfully. |

| No Real Estate Collateral: The invoices themselves are the security, meaning you don’t have to put up valuable business or personal assets (like property). | Loss of Control: (Primarily for Factoring) You hand over control of your collections process, which some business owners are uncomfortable with. |

6.2 The Lender’s Perspective: How Deals are Structured

Lenders need to mitigate risk, and they do this by carefully structuring the deal.

- Risk Mitigation: The financier’s biggest risk is that your customer doesn’t pay. They mitigate this by focusing on the creditworthiness of your customers (not you), setting a lower Advance Rate (e.g., 85% instead of 100%), and using Recourse clauses to pass the risk back to you where necessary.

- Structuring the Deal:

- Single-Invoice Financing: You only sell one, specific high-value invoice at a time. This is flexible and low-commitment.

- Full-Ledger Financing: You commit all your invoices (or all invoices from specific customers) to the financier. This offers higher overall funding but requires a longer commitment.

Invoice Financing vs. Other Working Capital Solutions

Before choosing invoice financing, it helps to see how it stacks up against other popular funding options:

| Solution | Speed | Cost | Collateral | Best For |

| Invoice Financing | Fast (24–48h) | Medium–High | Invoices | B2B with slow-paying, creditworthy customers. |

| Bank Overdraft | Days–Weeks | Low | Real Estate/Assets | Established businesses need short-term flexibility. |

| Business Loan | 1–4 Weeks | Low–Medium | Assets/Covenants | Long-term investments, large equipment purchases. |

| Merchant Cash Advance | Very Fast (24h) | Very High | Future Sales | B2C, retail, or restaurants that lack invoices but have daily card sales. |

| Equity Funding | Months | Dilution | None | High-growth startups need large capital and mentorship. |

6.3 The Indian Market: TReDS & FinTech Revolution

India’s working capital landscape is rapidly evolving, driven by government initiatives and technology.

The growth of TReDS is exponential: The value of invoices financed through TReDS has surged by over 1100% in five years (FY20 to FY24), unlocking more than ₹1.38 lakh crore for MSMEs in FY24 alone (Source Link ). This success validates invoice financing as a crucial financial tool.

Furthermore, studies show the direct business impact: TReDS has reduced the average receivable cycle for MSME suppliers by a remarkable 23 percentage points, leading to an estimated 8% increase in sales for participating firms (Source: RXIL Impact Assessment).

6.3.1 The Local Landscape: FinTech vs. Traditional Banks

The Indian market is now a battleground between slow, legacy processes from traditional banks and agile FinTech platforms. FinTech providers leverage technology to offer far faster approvals, easier onboarding, and specialised solutions (like confidential discounting) that banks often struggle with.

6.3.2 Key Development: TReDS (Trade Receivables Discounting System)

TReDS is a game-changer for Indian MSMEs. It is an RBI-regulated electronic platform designed to facilitate the financing/discounting of trade receivables (invoices) of MSMEs from corporate and government buyers through multiple financiers (banks/NBFCs).

- TReDS in 2025: The government has been actively pushing TReDS adoption. Companies with a turnover exceeding ₹250 crore and all Central Public Sector Enterprises (CPSEs) are now required to onboard the TReDS platform to ensure that MSME suppliers receive quick payments. This has cemented TReDS as the safest, most transparent way for MSMEs to manage receivables.

6.3.3 The Future is Automated: What’s New in 2025

The process of getting working capital is getting dramatically faster:

- AI-Powered Approval: Modern FinTech lenders use AI to analyse GST returns, e-invoice data, and bank statements, cutting approval times from days to under 24 hours. For example, ICICI Bank: AI in Loan Assessment

- Integration: Many providers now offer seamless integration with popular accounting software like Tally, Zoho Books, and SAP, allowing you to fund invoices directly from your existing system.

- Regulatory Focus: The RBI continues to update MSME lending guidelines, focusing on transparency and ethical lending, making the sector safer for small businesses.

7. How to Choose the Right Partner: Ensuring Success and Trust

You now know what invoice financing is, how it works, and which model (Factoring vs. Discounting) best fits your needs. The final, crucial step is selecting the right partner.

In the complex Indian financing ecosystem, the right partner is not just a lender; they are a strategic ally for your working capital management.

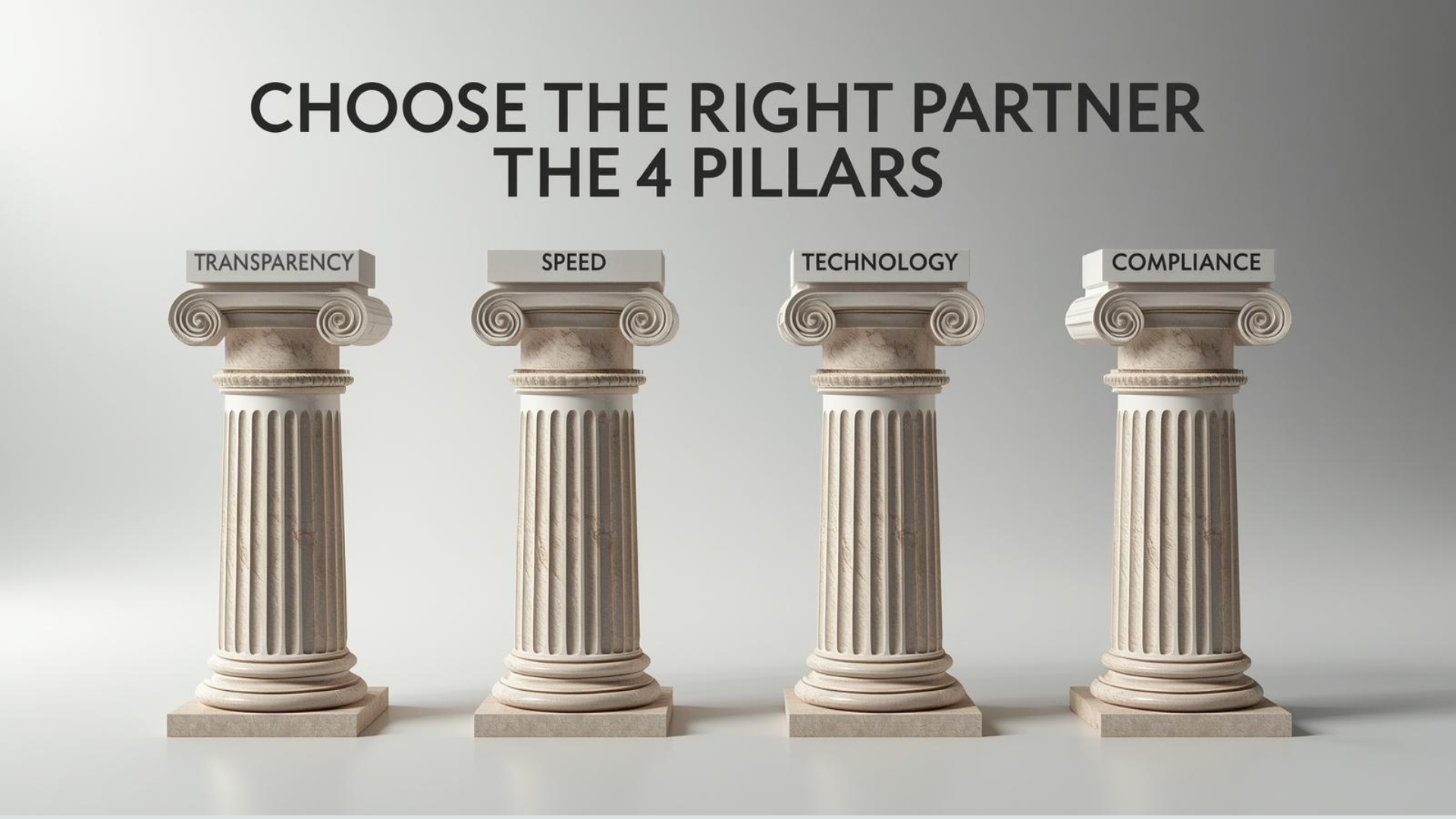

7.1 What to Look for in a Financier

When evaluating potential partners, look beyond the “lowest rate” and focus on these four pillars of trust and efficiency:

- Transparency: You want to see every fee right from the start. A partner you trust doesn’t hide costs in the details or hit you with surprises later. They just lay it all out what you’re paying, why, and when. No hidden fees. No confusing terms. Just clear, honest pricing, so you can actually make the right call for your business.

- Speed: How quickly can you actually get your funds? A reliable, tech-driven platform should move fast, getting your cash advance to you within 24 to 48 hours after approval. Because when business needs arise, every hour counts.

- Platform & Technology: Is the technology easy to use? Look for a user-friendly platform that integrates with your existing accounting tools (like Tally or Zoho) and allows for quick, digital invoice submission and tracking.

- Compliance & Local Expertise: Are they RBI-compliant? In India, navigating GST and regulatory requirements is essential. Choose a financier who is intimately familiar with the Indian market, MSME guidelines, and TReDS.

7.2 🚩 Red Flags: When to Walk Away

In the competitive world of invoice financing, certain practices are clear indicators that a financier may not have your best interests at heart. Always be wary of the following:

- Refusal to Disclose Total Fees: If a lender won’t tell you exactly what you’ll pay for setup fees, processing charges, the whole package, just leave. You need to know what you’re getting into, plain and simple.

- Personal Guarantees on Non-Recourse Deals: If you pick this type, the risk is on the lender, not you. So if they ask for a personal guarantee anyway, that’s a red flag. It goes against the whole point of a non-recourse deal.

- Lack of Online Presence or RBI Registration: If you’re dealing with a real company, you’ll find solid online reviews and proof they’re registered with the right regulators.

- Pressure to Sign Immediately: A reputable partner provides time for due diligence. Avoid any company that pressures you with same-day deadlines.

- Exorbitant Per-Invoice Fees: While a small processing fee is standard, charging an unreasonably high amount (e.g., above ₹500 per invoice) is a way to significantly increase the hidden cost of financing.

7.3 How MRKN Helps You Succeed

Given the complexities of the Indian market, choosing the right partner is critical. It’s not just about the lowest fee; it’s about speed, transparency, and local expertise.

“At MRKN, we streamline the working capital process for B2B businesses and MSMEs across India by offering a transparent FinTech platform that funds invoices in as fast as 24 hours.”

As this guide shows, the choice between factoring and discounting comes down to two things: confidentiality and control.

While factoring is a valid solution, we built MRKN for the businesses in “Scenario 2,” the established agencies, IT firms, and consultants who need funding without altering their client relationships.

Our platform is built on the three pillars you need:

- 100% Confidentiality: Your customers never know you are using financing. You maintain full control of your client relationships. This is the “Invoice Discounting” model, perfected.

- Transparent Speed: We provide a clear, upfront fee structure (unlike factoring’s complex charges) and use AI-powered approvals to fund your invoices in as fast as 24 hours.

- Local Expertise: We are fully RBI-compliant and offer seamless integrations with Tally and Zoho to fit your existing Indian workflow.

We don’t just offer a service; we offer the specific solution that protects your most valuable asset: your customer relationship.

8. Conclusion: Your Final Checklist & Next Steps

Momentum-killer? Nah. Your short-term cash gap is just a hurdle, not a wall. Invoice financing lets you grab the money you’ve already worked for turning approved sales into usable cash right when you need it. What seals the deal? Choosing the smartest financing method and teaming up with a partner who’s absolutely transparent, reliable, and actually gets your hustle.

The key to mastering your cash flow is understanding your core business needs: Do you value confidentiality, or do you need administrative support?

Your Final Invoice Financing Cheat Sheet

Use this simple table as a quick reference guide before you reach out to a financier:

| If Your Business Need Is… | Your Best Choice Is… |

| Help with collections & admin | Factoring (The full-service model) |

| 100% confidentiality | Discounting (The control model) |

| Bad debt protection | Factoring (Specifically Non-Recourse) |

| Full control of customer relations | Discounting |

Ready to Stop Waiting 90 Days to Get Paid?

You’ve done the research, you know the risks, and you know the rewards. It’s time to take action.

We are ready to partner with you to unlock your working capital.

Schedule a free, no-obligation cash flow analysis with our experts today. Discover how quickly we can turn your outstanding invoices into growth capital.”

❓ Frequently Asked Questions (FAQ)

1. Is invoice financing a loan?

No, invoice financing is not a loan. Invoice financing is an advance against money you have already earned (your accounts receivable). It is generally viewed as the sale of an asset or a working capital solution, not new debt on your balance sheet.

2. How much does invoice financing cost in India?

Invoice financing in India typically costs between 0.5% and 3% per month on the advanced amount. This equates to an annualised rate of 6% to 36%. Businesses should also budget for one-time setup fees, which usually range from ₹5,000 to ₹50,000.

3. What is the difference between factoring and bill discounting in India?

The primary difference is control and confidentiality:

- Factoring: The financier buys the invoice, manages the sales ledger, and handles all payment collections (not confidential).

- Bill Discounting: The financier advances cash, but you retain control of the sales ledger and manage collections (confidential). This is the mechanism often used on the TReDS platform.

4. Can startups get invoice financing?

Yes, startups can get invoice financing if their customers have good credit profiles. Since the invoice is the collateral, the customer’s creditworthiness is more important than the startup’s operating history. Most providers require a minimum of 6+ months in business and verifiable B2B invoices.

5. What happens if my customer doesn’t pay (Recourse vs Non-Recourse)?

It depends on the agreement type:

- Recourse Financing: If the customer fails to pay, you must repay the advance to the financier. The risk stays with your business.

- Non-Recourse Factoring: The financier assumes the risk of the customer’s financial inability to pay (e.g., bankruptcy). This feature comes with a higher fee.

6. How long does invoice financing approval take?

Approval times vary by provider:

- FinTech Lenders: Typically approve and fund within 24 to 72 hours.

- Traditional Banks: Approval and setup can take much longer, usually 2 to 4 weeks.

7. Do I need to finance all my invoices?

No. Most modern invoice financing providers offer selective (or spot) financing, allowing you to choose which specific invoices or customers you want to finance. You are not typically required to commit your entire sales ledger.

8. What industries use invoice financing the most?

Invoice financing is most popular in B2B industries with long payment cycles, including manufacturing, wholesale distribution, IT services, staffing and recruiting, and construction.

9. Is invoice discounting legal in India?

Yes, invoice discounting is legal and regulated in India. It falls under the purview of the Reserve Bank of India (RBI). The TReDS platform is a key government-backed mechanism for secured MSME invoice discounting.

10. What credit score do I need for invoice financing?

While your business’s credit score (CIBIL) should ideally be 600+, your customer’s creditworthiness is the most critical factor. Lenders focus on ensuring your customer has a strong payment history, typically requiring their score to be 650+.